Veeva Systems Inc provides cloud-based software tailored to the needs of the pharmaceutical, medical devices, healthcare and other life sciences industries. It offers consistent revenue and earnings growth and a wide moat with little direct competition.

Markel Industries is a specialty insurance provider that has built a high-quality investment portfolio and a group of profitable majority-owned business subsidiaries using its insurance float. Its effective adoption of the Buffet model has attracted a significant equity investment from $BRK.

______________________________________________________________________

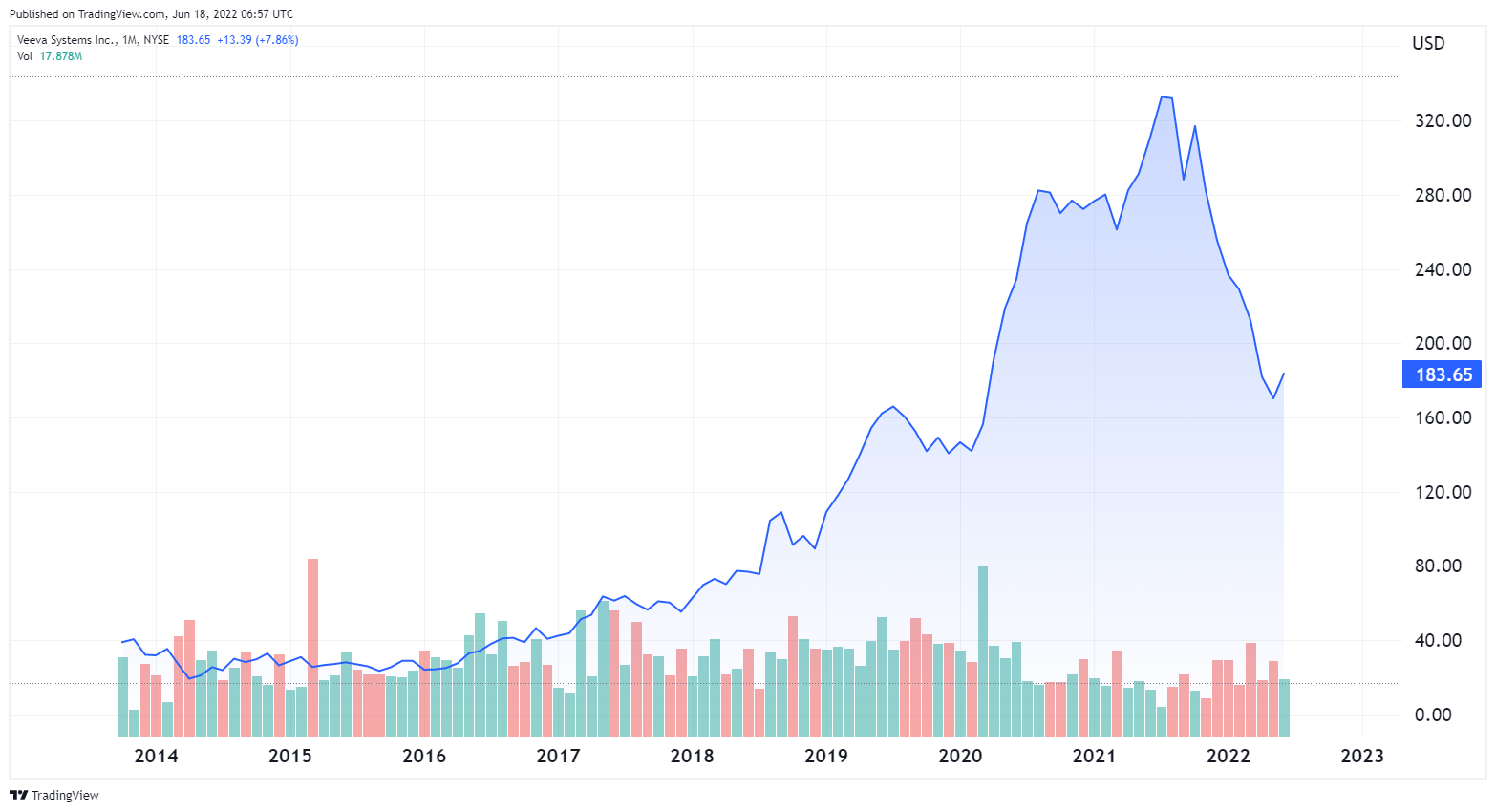

Veeva Systems Inc ($VEEV)

Source: tradingview.com

???? Summary:

- Share price at the time of writing: $187.50

- Veeva Systems Inc. supplies cloud-based software solutions specifically tailored for the global life sciences industry.

- Veeva dominates its niche and has customers in healthcare, pharmaceuticals, medical devices and allied industries all over the world.

- $VEEV has shown consistent revenue and earnings growth, with strong margins and return on equity.

- $VEEV is down 46% from its August 2021 peak in a general retreat by growth tech companies, despite continuing revenue increases in a highly resilient business.

???? What they do:

Veeva Systems Inc. is the leading provider of industry-specific cloud-based software for the life sciences industry.

The Company was founded in 2007, recognizing that the needs of this industry were unique enough to require tailored solutions rather than generic ones. Veeva now provides a range of software and consulting products and services covering the entire spectrum of life science business needs, from R&D to commercialization.

Veeva offers a wide range of products and services, including:

- Veeva Commercial Cloud is a suite of 17 software, data, and analytics solutions supporting sales, marketing, and medical affairs functions.

- Veeva Development Cloud is a 31-component solutions suite aimed at clinical trial, regulatory, quality, and safety functions, built into the proprietary Veeva Vault Platform.

- Veeva MedTech Suite offers connected cloud software solutions designed to speed up the MedTech product development, marketing, and distribution cycle.

Veeva also offers specific solutions for the Consumer Products & Chemicals (CP&C) industry, along with business consulting and professional services and support.

During the fiscal year ending January 31, 2022 Veeva generated 56% of total revenues from commercial solutions and 44% from development solutions.

Veeva served 1,205 customers as of Jan. 31, 2022, ranging from global pharmaceutical giants to emerging development-stage biotech and pharmaceutical companies. Prominent customers include Bayer, Pfizer, GlaxoSmithKline, Johnson & Johnson, Moderna, Novartis, Janssen, Bristol Meyers Squibb, AstraZeneca, Eli Lilly, Genentech, and Sanofi

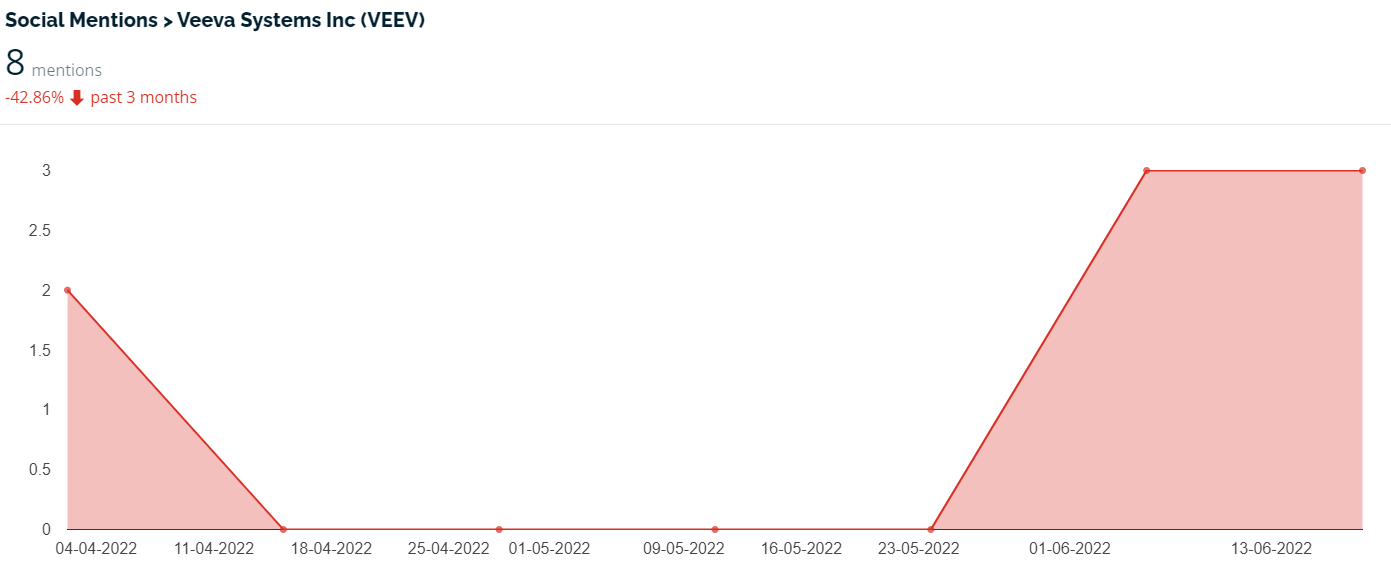

???? What we learned from social media and institutional investment patterns:

Veeva received some attention on social media in 2020 and 2021, while shares surged from $120 to a peak of $340. More recently the attention has completely lapsed, with only 8 mentions in the last 3 months. Even an exceptionally positive earnings release on June 1 generated only minimal attention.

One Reddit member posted a link to earnings discussion, but it received no responses and no visible attention, indicating a minimal level of social media attention.

This may be part of a general turndown in activity on stock discussions as markets slip into bear market territory. It may also be related to a very high level of institutional ownership, which Nasdaq reports at 88.55%. Either way, retail investor interest appears to be minimal.

$VEEV has a high concentration of institutional ownership. CNN Business reports that individual stakeholders own only 1.86% of the shares. Leading institutional holders include mutual fund giants T. Rowe Price, Vanguard, Blackrock, and Morgan Stanley.

The low level of retail investor ownership may be caused by the general retail bailout from growth shares and by the general obscurity of the company: very few individual investors have ever heard of Veeva Systems or its products.

???? Smart Money Signal: Prominent holders of $VEEV shares include Ray Dalio with 389,000 shares and Cathie Wood with 250,000. Both Dalio and Wood made large purchases as share prices tumbled in Q1 2022.

???? Why $VEEV could be valuable:

The global life sciences analytics market is expected to show a CAGR of 7.7% through 2030.

Veeva sits at the intersection of two rapidly emerging macro trends: technology-driven healthcare development and cloud computing. Veeva faces no direct competition in life science-specific cloud software.

Data management is emerging as a critical requirement for the life sciences industry. The Deloitte 2022 Global Life Sciences outlook, for example, stresses the need for companies to transition from “going digital” to “being digital”. This is precisely the challenge that Veeva’s products address.

Veeva serves an industry that is known for being recession-resistant. Healthcare is not a discretionary expense, and activity carries on even during economic downturns. There may be less business from startups and early stage companies, but the core business should endure.

Combining the entire range of Veeva software into Veeva Cloud, with a common system architecture, provides a huge incentive for customers using one or more Veeva products to use more as their needs expand.

Veeva claims to hold 80% of the life sciences Customer Relationship Management (CRM) software market, with 19 of the the 20 top pharmaceutical companies using its products.

Veeva has an enormous moat: once a client has invested in Veeva software it would be a huge challenge to switch to a competing system. The sensitive nature of the work, reluctance to adopt an untried product, and the extremely strict regulatory requirements are a high bar to cross for any potential emerging competitor.

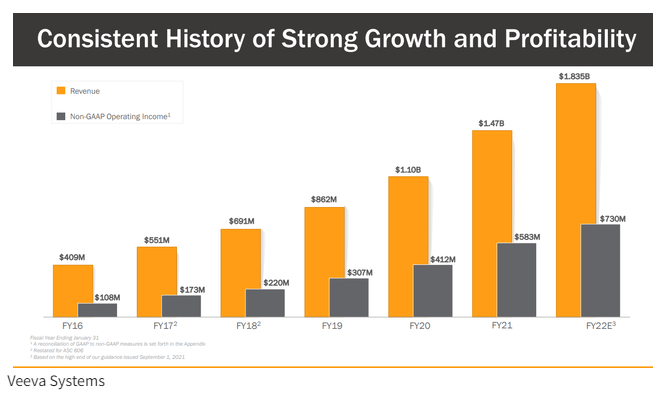

Veeva has steadily increased revenues and earnings for the last six years, with no interruption from the COVID-19 pandemic.

Source: finnoexpert.com

After revenues increased 26% and earnings rose 27% in FY 2022, Veeva worried some investors by announcing that it expected that FY 2023 would see revenues increase by only 17% and earnings by 8%, a consequence of large R&D deals that would take longer than usual to realize as revenue and of a general slowdown in the business environment.

That announcement sent some investors into retreat. While the figures do represent the slowest growth since Veeva’s IPO in 2013, they also represent a level of revenue and earnings growth that many companies would consider an achievement in the midst of a general economic downturn.

Veeva has a solid operating margin of 26.26%, reasonable return on equity at 14.94%, and cash exceeds debt by a wide margin, leaving the company effectively debt-free.

$VEEV has beaten analyst consensus earnings targets for four consecutive quarters.

$VEEV holds a consensus “buy” rating from 14 analysts. The average price target is $214.50, 16.8% above the price at this writing.

Veeva Systems stock is down 46% since its August 2021 peak of $340.98, despite continued impressive results. The decline appears to be driven urely by an overall negative market perception of high-growth technology stocks rather than by any issues with the company.

⚠️ What the risks are:

1️⃣ Valuation remains a concern. Veeva Systems has long carried a premium valuation characteristic of consistently profitable high-growth tech companies. Even after a 46% dive in price the forward P/E is still 44.32. This is not a value stock by any means, and if market conditions continue to deteriorate the price could slip further.

2️⃣ Growth may be impaired by economic conditions. Veeva’s core business is highly-recession-resistant, but customer growth and new projects could be significantly impaired by recession or continued bear market conditions. Failure to meet growth targets could have a significant impact on the stock price.

3️⃣ Any product failure could have a large impact on the business and the stock price. Veeva systems products help customers navigate extremely complex regulatory processes in multiple markets and handle large amounts of highly confidential data. Any data breach or operational failure could expose the company to significant liabilities and damage the reputation that they rely on to attract and retain customers.

Bottom line: $VEEV is a high quality, resilient, consistently profitable growth company trading at a discount at a time when growth stocks are unpopular. Long-term investors looking for growth stock deals will want to take a detailed look at the company.

Markel Corporation ($MKL)

Source: tradingview.com

???? Summary:

- Share price at the time of writing: $1282.20

- Markel Corporation is a leading provider of specialty insurance products.

- Markel also manages an active investment portfolio and owns controlling interest in a diverse portfolio of businesses.

- Markel’s structure is often compared to that of Berkshire Hathaway, and BRK recently purchased a $620 million stake in Markel and BRK is Markel’s largest equity holding.

- Revenues and earnings have grown steadily and the valuation remains highly attractive.

???? What they do:

Markel Corporation has been in business since 1930. It is a financial holding company, operating in three divisions.

- Insurance: Markel is a leading provider of specialty insurance products, combining extensive experience with cutting edge technology to match risk and capital profitably.

- Investments. Like Berkshire Hathaway, Markel invests its insurance float, and has a history of doing so very effectively.

- Markel Ventures: Markel makes regular acquisitions and owns controlling interests in multiple businesses outside the insurance industry.

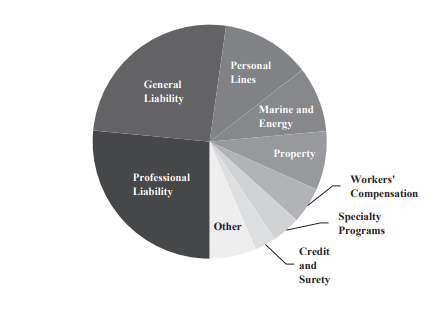

Markel’s insurance division works with, insurance, reinsurance, and insurance-linked securities. It provides insurance for specialized professions, facilities in specific industries, classic cars and watercraft, marine industries, and other lines that many companies lack the expertise to price effectively.

These markets are less price-sensitive and allow higher margins. This is a breakdown of Markel Insurance sector exposure:

Markel’s investment portfolio includes shares in a wide variety of publicly traded companies. The leading holdings are Berkshire Hathaway A, Berkshire Hathaway B, Brookfield Asset Management, Alphabet, Amazon, Deere, and Home Depot.

The portfolio may fluctuate with market conditions and with insurance conditions. If management believes that a larger cash position may be required to cover liabilities (in the event of a major natural disaster, for example) they may choose to liquidate stock holdings.

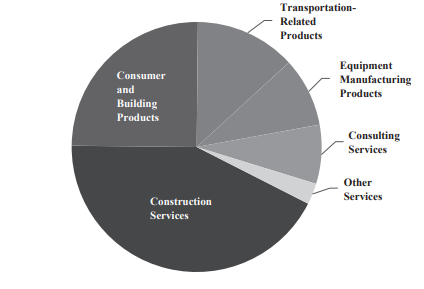

Markel Ventures holds majority interests in 20 different companies. Market makes regular acquisitions, focusing on profitable businesses with strong growth potential.

Markel Ventures holds companies in these sectors, broken down by revenue.

Markel Ventures acquired Metromont LLC and Buckner Heavy Lift Cranes in 2021, Lansing Building Products, LLC in 2020, and VSC Fire & Security in 2019, accounting for part of the division’s revenue and income growth.

???? What we learned from social media and institutional investment patterns:

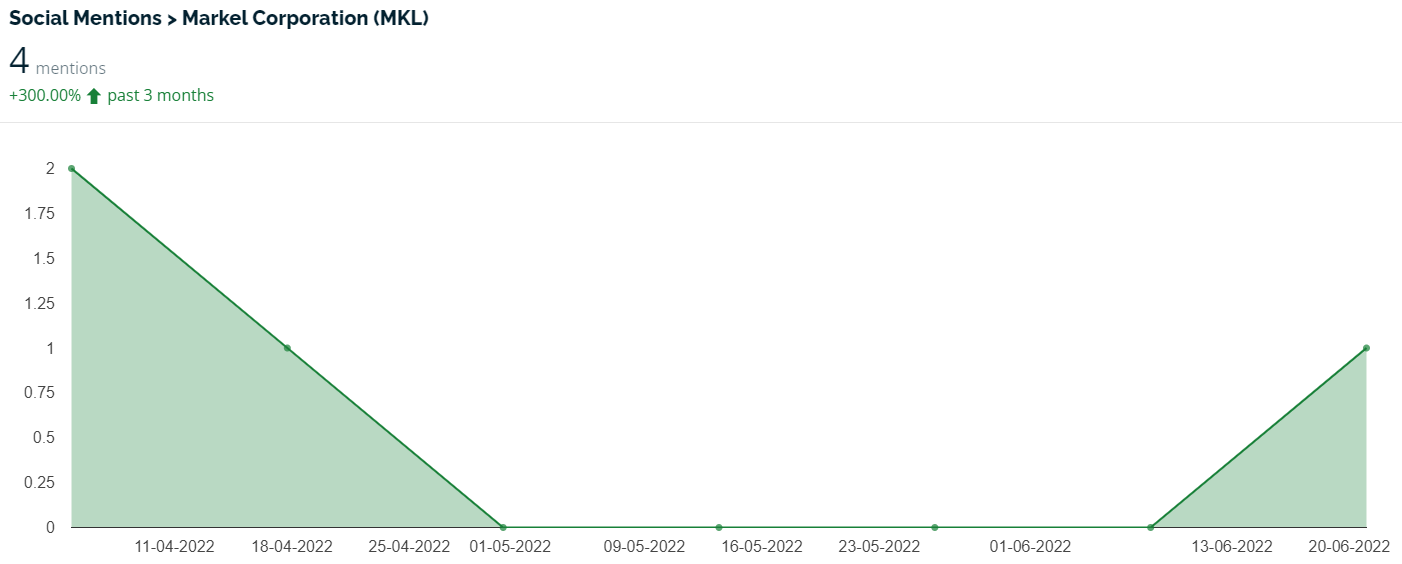

Markel Industries is virtually invisible on social media. In some ways that’s not surprising: it’s what many Reddit investors would consider a “boring stock”, and it’s certainly not a stock that’s ever going to “go viral”.

The lack of attention is also surprising in some ways. With growth stocks falling like stones and a renewed level of attention toward value investing, we’d expect Markel to get some attention, if only for its similarity to the Berkshire Hathaway business model.

Either way, the numbers speak for themselves: 4 mentions in three months is a very low level of attention, though there is one generally positive Reddit thread on r/valueinvesting just over 3 months ago.

Just over 80% of the Markel float is held by institutional investors with Vanguard the leading holder with 1.18 million shares, over 9% of the float.

Notable Comments from Reddit:

“Tom Gayner is one of the greatest investors that nobody knows about. He is very careful with his management of the portfolio and I have the utmost confidence in Markel long-term.”

– Revfunky

“I would consider MKL a very good business selling at a reasonable price right now. Not selling with a large margin of safety but still a solid investment compared to the overall high valuations on most companies within the current market.”

– williamsdavida9000

???? Smart Money Signal ???? Warren Buffet’s Berkshire Hathaway purchased 420,000 shares of $MKL in Q1 2022.

???? Why $MKL could be valuable:

The specialty insurance market is expected to grow at a CAGR of 9.3% through 2030, as clients look for tailored rather than generic insurance products.

Markel’s equity investments span a range of industries, but their majority owned portfolio has a concentration in construction and building materials, which are projected to grow at a CAGR of 3.7% through 2025 and a CAGR of 4.9% through 2028 respectively.

Markel CEO and Chief Investment Officer Tom Gayner is a highly experienced value investor with an impeccable reputation and a track record of producing consistent gains over extended periods of time.

Markel’s substantial portfolio of profitable privately owned companies gives shareholders a direct ownership stake in companies that are not publicly traded and not overvalued by the market.

Markwel’s core insurance business is expanding rapidly. Gross written premiums increased 18% in 2021 and underwriting profits were up 390%. Markel’s experience in pricing and client selection has allowed the company to navigate frequent natural disasters and an increasingly litigious environment and maintain profit growth.

Markel Ventures now owns 20 companies, with combined operating revenues of $3.6 billion.

Markel’s equity portfolio returned 29.6% in 2021, better than the S&P 500’s 26.89% despite a relatively risk-averse investing philosophy.

Overall operating revenues rose 28% in 2021 over 2022, with margins rising to 25.2% and net income surging 198%.

Markel’s growth is not a short-term phenomenon. Since 2012 operating revenues have more than tripled from $3 billion to over $9.7 billion. Markel’s 10-year revenue CAGR is over 15%.

Cash holdings exceed debt, leaving the company effectively debt-free.

Despite its long-term growth trend, Market remains very reasonably valued, with a trailing P/E just over 10, the 5-year expected PEG ratio at 0.89, and price to sales at 1.41.

Markel’s extremely small float – under 13 million shares – enables the share price to rise steeply on even a relatively low level of buying.

⚠️ What the risks are:

1️⃣ Markel is highly dependent on the services of Co-CEO and Chief Investment Officer Thomas Gayner. The company could see a serious long-term impact if Gayner is unwilling or unable to continue in these roles.

2️⃣ $MKL revenue and earnings growth is traditionally “lumpy”: some quarters are excellent, some good, some poor. While the long term record is consistently positive, short-term negative growth could drive share prices down.

3️⃣ Markel’s insurance business is vulnerable to natural disasters, and one or more high-impact disasters occuring during a bear market could force Markel to liquidate investment holdings at a significant loss, affecting results.

Bottom line: Markel is a largely under-the-radar value play with an inflation-resistant business, a very strong management team, and a track record of solid decisions and long-term growth..