Summary

Microsoft is a dominant tech company that has consistently outperformed major indices and is now trading at a highly accessible valuation. A wide moat and extraordinarily solid financials place the stock as both a blue chip and a growth tech investment.

Twilio provides widely used cloud communications tools. Bid up to insane levels during the pandemic craze for anything related to remote work, the stock was left for dead in 2022, tumbling to its lowest levels since 2018 even as revenues soared.

______________________________________________________________________

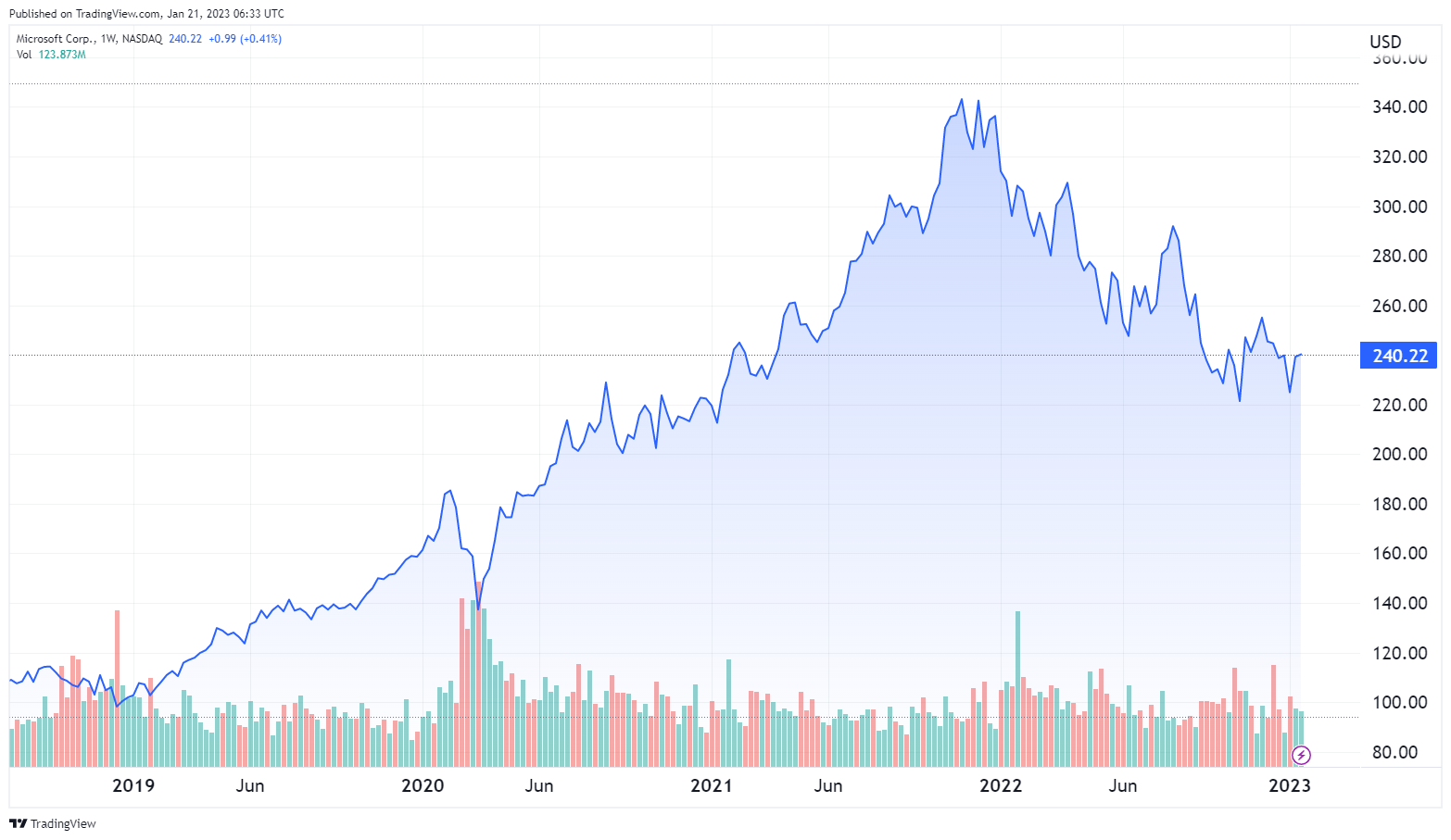

Microsoft Inc. ($MSFT)

Source: tradingview.com

???? Summary:

- Share price at the time of writing: $240.22

- Microsoft is the world’s largest software company, with a dominant position in personal, enterprise, and cloud computing.

- $MSFT produces a huge range of software products, competing in multiple industries.

- The Company generates enormous cash flow, supporting a steady stream of acquisitions and a significant dividend.

- $MSFT shares are trading at 30% below their November 2021 peak despite rapidly growing revenue and earnings.

???? What they do:

Microsoft is a global producer of software, services, devices, and related solutions. It is currently the world’s largest software company by a wide margin.

$MSFT sells through OEMs, resellers, and distributors, with direct sales through digital marketplaces, online stores, and physical retail outlets.

Microsoft operates in three reportable segments.

The Productivity and Business Processes segment includes:

- Office Commercial, including Office 365, Office, Exchange, SharePoint, and Viva.

- Office Consumer, including Microsoft 365 subscriptions, Office on-premises licenses, and other Office services.

- LinkedIn, including Talent Solutions, Marketing Solutions, Premium Subscriptions, and Sales Solutions.

- Dynamics Business Solutions, a set of intelligent, cloud-based applications across ERP, CRM, Customer Insights, Power Apps, and Power Automate; and on-premises ERP and CRM applications.

The Productivity and Business Processes segment provided 32% of revenue in 2022

The Intelligent Cloud segment includes:

- Server Products and Cloud Services, including Azure, SQL Server, Windows Server, Visual Studio, System Center, Nuance, and GitHub.

- Enterprise Services, including Enterprise Support Services, Microsoft Consulting Services, and Nuance professional services.

The Intelligent Cloud segment provided 36.4% of revenue in 2022

The More Personal Computing segment is focused on individual consumers, including:

- Windows is the world’s most popular single operating system for personal computers.

- Devices include Surface and PC Accessories.

- Gaming includes XBox hardware, content and services, and XBox Cloud Gaming.

- Search and Advertising delivers relevant search, native advertising, and display advertising to clients worldwide.

The More Personal Computing segment provided 30% of revenue in 2022

Each of these divisions contains its own range of products and services, and many could be major companies in their own right.

Microsoft sells its products both through outright sales and licensing agreements that generate recurring revenue.

Microsoft’s operations generate large amounts of cash, and the company routinely uses that cash for acquisitions. As a result, Microsoft is one of the most acquisition-oriented companies in the world.

Since January 2020, Microsoft has fully acquired 22 different companies, including the 2022 purchase of game maker Activision Blizzard for $68.7 billion. MSFT also purchased a 4% stake in the London Stock Exchange in 2022, part of a multi-billion dollar deal to develop data analytics and cloud technology.

Microsoft is currently in talks to invest $10 billion in OpenAI, the owner of the ChatGPT AI platform.

???? What we learned from social media and institutional investment patterns:

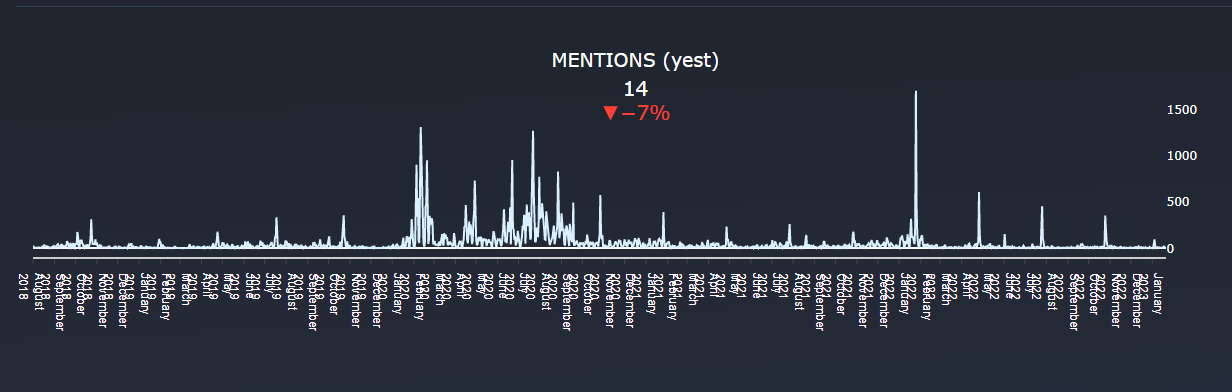

$MSFT is a staple of online stock discussion, routinely appearing in lists of the top trending stocks on social media. The company’s dominance of a leading tech sector, enormous moat, gargantuan cash flow, and household-name status are impossible to ignore.

While MSFT is a constant topic of conversation, there’s no evident uptrend or downtrend. There’s a steady level of talk that spikes quickly to very high levels on any news. Microsoft is closely watched by the media and is considered a bellwether for the tech sector, so news is widely distributed and spreads quickly.

Source: quiverquant.com

Microsoft is obviously in the public eye and the stock price reacts quickly to company news or broader economic news.

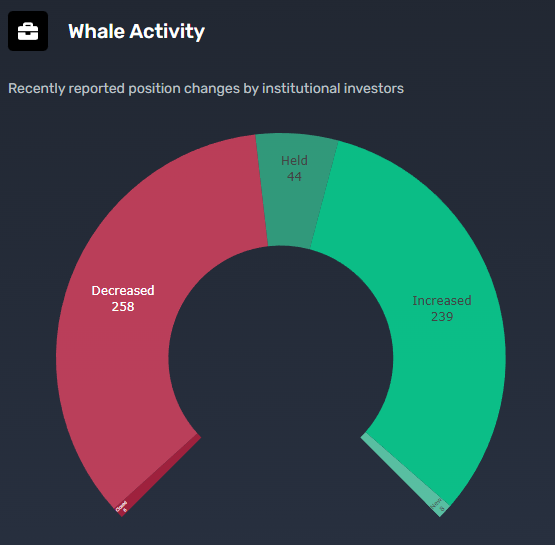

Institutional investors hold 73.37% of the $MSFT float, led, as usual, by Blackrock and Vanguard. This is a relatively low level, especially considering the large number of shares held by market cap-weighted index funds.

Institutional investors that are actively trading $MSFT seem to have a relatively neutral view, with sales and buys closely equal. Note that while 5,966 institutions hold shares, only 547 reported recent position changes.

Source: quiverquant.com

Notable comments from Reddit:

“Been in MSFT for the last 3 years and I can for sure tell it is my favourite stock pick since it provides me with a superior combination of the following characteristics:

- Great returns / growth

- Peace of mind – Too big to fail, tech giant that keeps innovating and growing, great balance in various tech related fields, could say similarly close with an ETF

- Continuously and consistent dividend that grows up over the years

Definitely one of the very few companies on my radar that meets the term “buy it and sleep”, so I will continue building a bigger position on it now and if it continues I will load even more :)”

– nickath 42

“MSFT is the dark horse that dominates every bit of technological advancement. They’re poised to win in the long term be it in Cloud, Consumer, Productivity, Cybersecurity, R&D, Defense, Gaming, Healthcare, Marketing (Ad Tech) and so on. It’s well diversified conglomerate of businesses that produces tons of cash flow.”

– dino_asteroid

???? Smart Money Signal: Ken Fisher of Fisher Investments has bought MSFT for 11 consecutive quarters with no sales, and now holds 29 million shares.

???? Why $MSFT could be valuable:

Microsoft operates in high-growth markets. The software products market is expected to show a 12% CAGR through 2027. The enterprise software market is projected to grow at an 11.5% CAGR through 2030, and the cloud computing market is seen surging forward at a 17.9% CAGR through 2027.

Microsoft enjoys a dominant position in many of its markets, with millions of business and personal users already committed to its products. That creates one of the largest moats in the software industry.

Microsoft is one of the most diversified companies in the software industry, with leading positions in operating systems, cloud computing, productivity software, video games, social media, and digital advertising. That diversity insulates the company against downturns in any single sector.

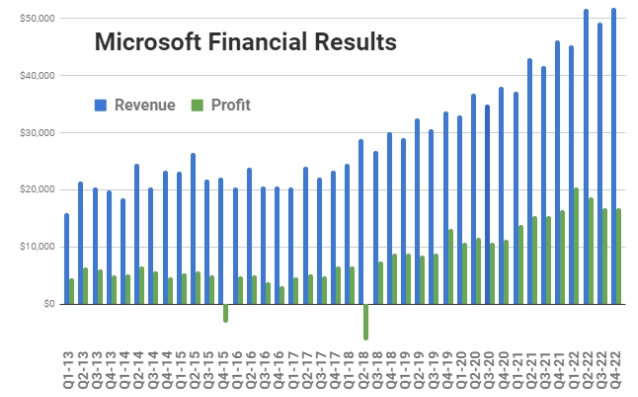

The importance of that insulation is demonstrated by results in the most recent quarter. The “More Personal Computing” segment reported a 15% year-on-year decline in operating income, driven by a cyclic downturn in PC sales. In the same quarter, though, the Intelligent Cloud segment posted a 20% growth rate and the Productivity segment grew 9%, enabling an 11% overall growth rate.

Microsoft Azure has a 21% market share in the booming cloud computing business, second only to Amazon Web Services. The company recently announced plans to build Azure data centers in 11 new regions.

Microsoft is rated #5 on the Chicago Tribune’s list of the best-paying companies in the US and #13 on Glassdoor’s list of the best workplaces in the US. The ability to attract and retain high-quality employees is a key competitive advantage.

$MSFT is the fourth-largest R&D spender in the US, and also pursues R&D through acquisition, acquiring companies that have developed compatible technologies. The company has an exceptionally strong record of selecting and integrating acquisitions.

$MSFT is extraordinarily profitable. Its operating margin is 41.69%, and return on equity is 42.88%. The company’s $107 billion cash hoard exceeds its $77 billion debt by a wide margin, and its S&P bond rating is AAA.

That financial solidity places $MSFT in a prime position to weather even a severe economic downturn. Results might suffer but competitors are likely to suffer more, leaving Microsoft in a better competitive position.

Revenues and earnings have been on a consistent uptrend since 2018. Not every quarter sees an increase, which may upset investors focused on the most recent number, but the overall trend is solidly up.

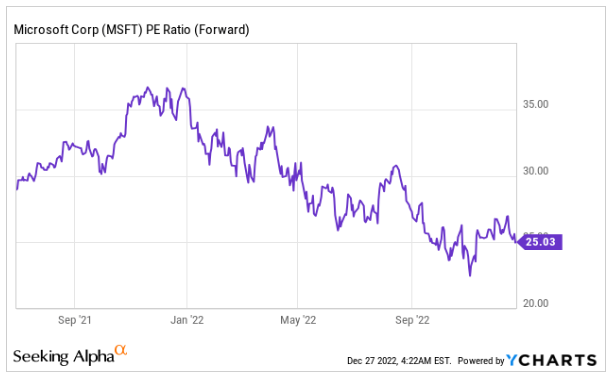

$MSFT shares were substantially sold off in 2022 in a general market retreat. The current P/E ratio of roughly 25 is well below historical averages and is arguably good value given the company’s financial strength and growth potential. Microsoft also pays a 1.17% dividend, a rarity among tech majors.

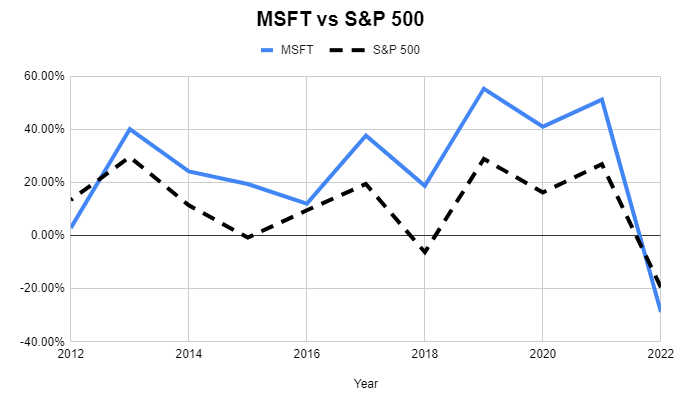

2022 was the first year in the last decade when $MSFT failed to outperform the SPX. There’s a high probability that this outperforming role will return as markets return to expansion.

34 analysts currently cover $MSFT. 14 rate it “Strong Buy” and 13 rate it Buy”, for an overwhelmingly positive view. The average analyst price target is $291.81, 21.5% above the current level.

⚠️ What the risks are:

1️⃣ Cloud Competition. Microsoft has invested heavily in the cloud computing market. This is one niche where they can’t rely on pre-existing dominance, and the competition comes from equally well-funded titans like Amazon and Google. There’s no assurance that Microsoft can achieve the kind of dominance in cloud computing that it has in other sectors.

2️⃣ Acquisition uncertainties. Microsoft is in the process of making its largest acquisition ever, a $69 billion move for Activision Blizzard. The acquisition is encountering questions from antitrust regulators in Europe and facing legal action in the US. If the acquisition is blocked, it could affect both the share price and Microsoft’s plans to expand its gaming market

3️⃣ Global status. Microsoft’s status as a global company has advantages but also risks. The company’s software products are routinely pirated in markets with poor intellectual property protections. The strength of the US dollar has acted as a drag on the value of foreign earnings, and while only 1.8% of revenues come from China, the company is still vulnerable to risks from China-Taiwan or China-US conflict.

Bottom line: After the 2022 selloff, many investors are searching for oversold quality companies. $MSFT fits this description. The company’s financial strength, market dominance, and long history of above-average returns make it a top target for investors seeking bear-market bargains.

Twilio Inc ($TWLO)

Source: tradingview.com

???? Summary:

- Share price at the time of writing: $54.26

- Twilio develops and sells cloud communication tools with a wide range of applications..

- Twilio’s products are used across a huge range of industries, insulating the company against single-sector downturns..

- The share price skyrocketed to irrational levels in 2020/2021 and fell 87% in 2022.

???? What they do:

Twilio is the developer of a leading cloud communication platform, giving software developers the tools they need to connect businesses with customers. Twilio develops Application Programming Interfaces (APIs) that allow different forms of software to communicate seamlessly.

Twilio’s APIs allow developers to embed voice, messaging, email, and video capabilities into their software, allowing applications to communicate with any connected device.

As of their last reported quarter, Twilio had over 280,000 active customer accounts across a huge range of businesses.

Twilio has multiple product lines, including:

- Twilio Flex is a comprehensive contact center management system, enabling multi-channel customer service with either distributed or centralized agents and reducing service times.

- Conversations API allows scalable, multiparty conversations integrating almost any current communications platform.

- Elastic SIP Trunking allows scalable, flexible, global voice communications on a pay-as-you-use basis, with no contracts or port/channel fees.

- Twilio Engage is a personalized customer engagement that allows full customer data management and personalized campaigns, reducing customer acquisition and retention cost.

- Twilio Frontline is a mobile CRM app designed to let employees manage customer relationships efficiently from any location.

- Security solutions include identity verification and other fraud protection methods.

- Programmable Wireless solutions connect IoT devices to global cellular networks.

Different clients use these systems in very different ways. Some examples:

- Airbnb uses Twilio’s systems to generate automated SMS messages linking hosts to guests, confirming bookings, and resolving issues.

- Dell uses Twilio APIs to reduce customer support escalations and increase sales.

- Chime uses multiple Twilio solutions to power its customer service system.

- The City of Pittsburgh uses Twilio’s products to run its 311 system for information and complaint resolution.

- Wise and Stripe use Twilio’s identity verification systems to protect customer accounts.

- Lyft’s customizable call centers are based on Twilio’s software.

- Toyota turned to Twilio to power its Drivelink connected-car architecture.

Almost any enterprise that needs to communicate with customers, suppliers, or other entities in a fashion that combines automation, personalization, and data management is a potential customer.

While the average consumer has never heard of Twilio, almost all of us have uses their products to communicate with or receive communications from a business.

???? What we learned from social media and institutional investment patterns:

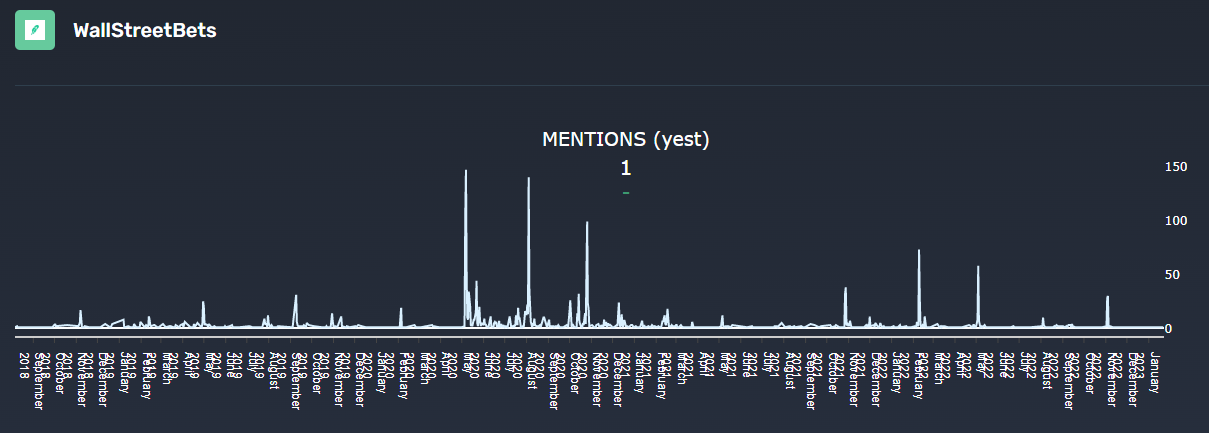

Twilio had some busy days on r/wallstreetbets in 2020 and 2021, when the stock soared 440% in less than a year. As with many of the pandemic darling stocks, attention and conversation dwindled to near-zero as the stock fell out of favor and the share price dove.

Source: quiverquant

There’s a bit more discussion on r/stocks, which seems evenly divided between investors who think the stock is wildly oversold and about to reach profitability and those wary of the company’s persistent inability to turn a profit.

While the stock belongs to a currently out-of-favor category and is not likely to be trending any time soon, that could change if growth tech cycles back into favor. Retail investors seem to be waiting for some indication of such a change before making moves.

86.74% of the Twilio float is held by institutions, led by Vanguard, Blackrock, and FMR. Recently reported changes tend toward the positive. This is a fairly common institutional investment profile and does not provide any strong indication in any direction.

Source: Quiverquant

Notable comments from Reddit:

“TWLO is critical tech saas infrastructure going for dirt cheap. The only reason they’re unprofitable is because they have aggressively pushed for growth year after year. This is a business that can easily become a high margin monster.”

– dCrumpets

“What's most important about TWLO is that they are essentially the backbone of automated communication services and lots of call centers. They are not going anywhere, and I only see growth in their future, financials be damned for now.”

– AliveInTheFuture

???? Smart Money Signal ???? Cathie Wood has purchased 3.3 million shares of $TWLO in the last four quarters, and now holds 6.83 million shares.

???? Why $TWLO could be valuable:

The cloud communication platform market is expected to grow at an exceptional 15.7% CAGR through 2030.

Twilio’s products are used across an enormous range of industries. Existing customers range from banks, car manufacturers, and governments to medical, food sercice, and hospitality. That variety gives some insulation from economic slumps in specific sectors.

Twilio’s revenues have grown consistently.

While revenues have grown consistently, the rate of growth has dropped. In Q3 2022 growth over the equivalent quarter last year was “only” 33%. Slowing growth rates are inevitable as the company matures, and many companies would envy a 33% growth rate, but investors have still reacted negatively.

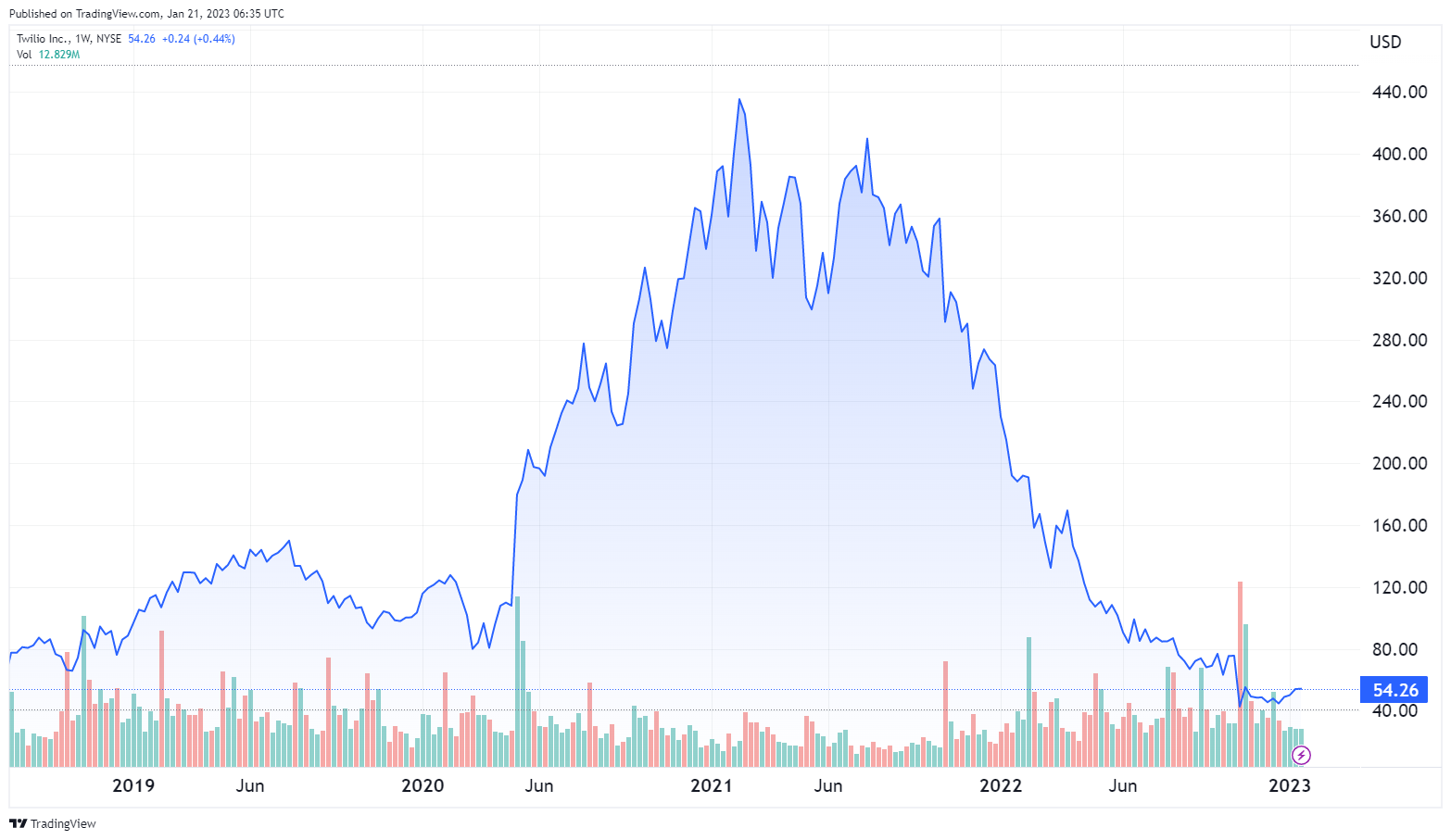

Twilio’s stock price movements have been completely separated from the company’s fundamentals. The stock went on an unprecedented run in March 2020, surging from $80.69 to $435.29 for a 440% gain in a single year.

When the momentum ran out the pandemic darlings quickly became pariahs, and Twilio shares quickly tumbled back to $54. The question for investors is whether the selloff has left the stock at an attractive entry point.

At the center of this question is Twilio’s profitability problem. Twilio is not only unprofitable, it has a negative margin: the more revenue the company brings in, the more money it loses. As long as that’s the case, investors are going to be wary.

If that changes, Twilio is likely to be a prime target as investors cycle back to growth tech. With the stock trading at only 1.6x next year’s sales forecast, even a substantial move in the direction of profitability is likely to bring the stock back onto the radar of investors.

One big plus for the company is its $4.21 billion in cash, almost $3 billion more than its debt. This gives the company the ability to carry several more years of losses before it rus into serious financial trouble.

Twilio’s CEO has explicitly stated that the long-stated goal of profitability in 2023 is still achievable and that the Company is “laser-focused” on achieving it. The Company has laid off 11% of its workforce and made other moves aimed at increasing efficiency, but the impact on the bottom line has yet to be seen.

The investment case for Twilio revolves almost entirely around their ability to fulfill that promise.

Tha analyst community appears to believe that they can do exactly that. Of 36 analysts covering Twilio in December, six rated it a “Strong Buy”, 14 said “Buy”, and 15 said “Hold”. The average price target is $81.37, 50% above current levels.

⚠️ What the risks are:

1️⃣ Current unprofitability. Twilio’s losses have accelerated at the same level as its revenues. Management has promised to reverse that in the next year. If they don’t deliver, investor confidence is likely to reach a breaking point.

2️⃣ Stock-based compensation. Twilio has relied heavily on stock to compensate its employees, issuing $793 million worth of stock in the last year alone. That policy has pushed shares outstanding steadily higher, diluting existing shareholders. If the company achieves profitability it can use some of its cash hoard to buy back shares, but that is not assured.

3️⃣ Economic headwinds. A general economic downturn could reduce spending on new technology among Twilio’s customers. That could slow revenue growth and make profitability harder to achieve.

Bottom line: Twilio is a speculative investment. It has the appeal needed to draw major gains in an expanding market, the company’s diverse customer base and steady revenue growth are impressive, and the stock has been heavily sold off. All that’s missing is profit. If management delivers on that promise the results could be spectacular. If it can't, the selloff may continue.

That's a wrap!

Don't miss our next report. If you haven't already make sure to whitelist this email so we don't end up in your promotions folder. Not sure how to do it? Use this guide.Got 15 seconds? To make sure we can keep improving Ticker Nerd we need to hear from you. We have a few quick questions for you here.