Public Storage is the largest provider of self-storage space in the US. The company is expanding rapidly and growing revenue and earnings, while the share price remains depressed.

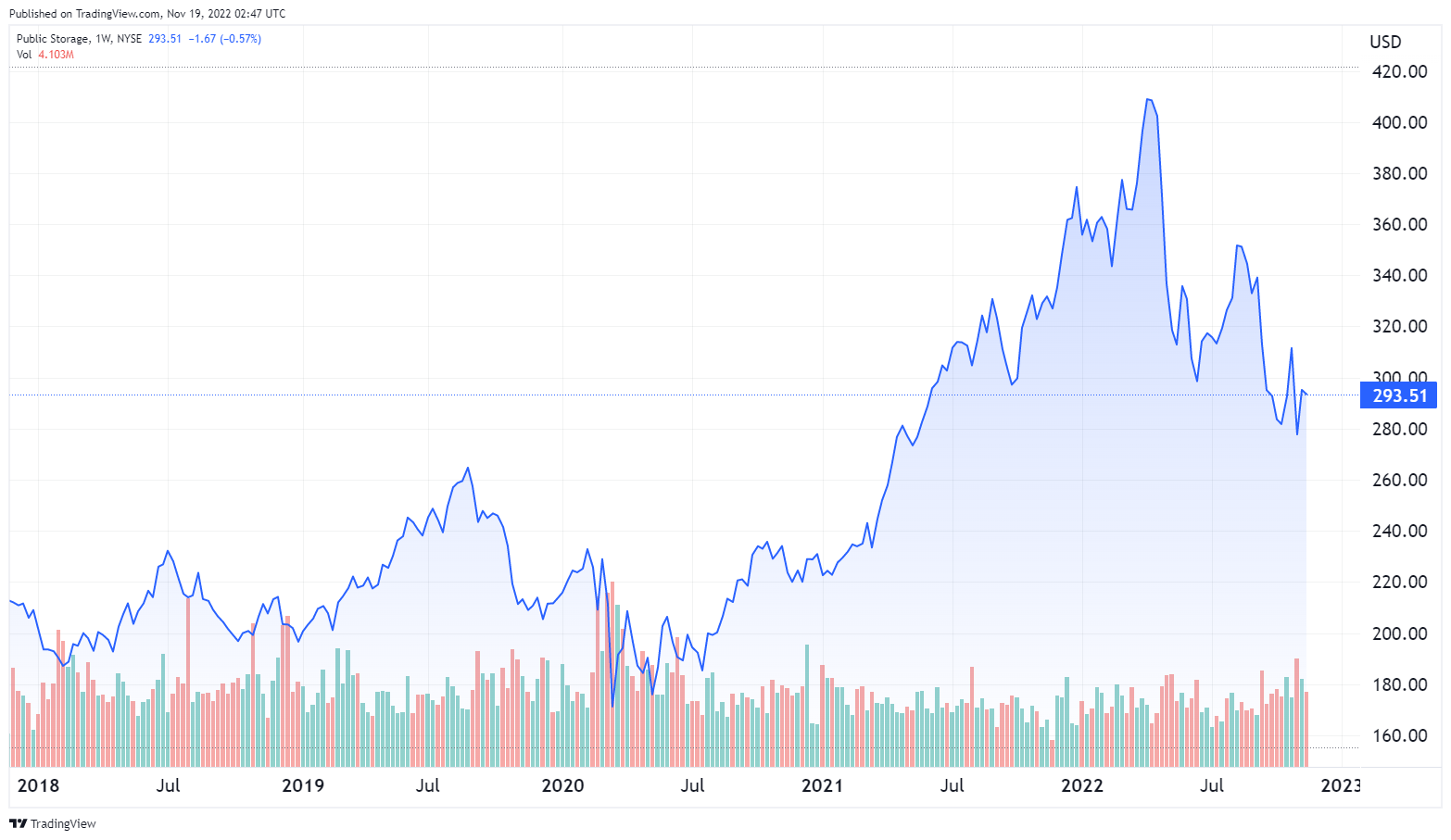

Public Storage Inc. ($PSA)

Source: tradingview.com

???? Summary:

- Share price at the time of writing: $293.51

- Public Storage is the largest self-storage REIT in the US, with 186 million square feet of rental space in 39 states.

- Since 2019 $PSA has added 26 million square feet of new storage space.

- Public Storage has shown consistent growth in revenue and funds from operations (FFO)

- $PSA shares are trading at 30% below recent peaks despite consistent strong financial performance.

???? What they do:

Public Storage is a Real Estate Investment Trust (REIT) specializing in self-storage space. The Company has been in business for 50 years and is the largest self-storage REIT in the country.

Like all REITs, Public Storage is required to distribute 90% of its taxable income to shareholders as dividends.

Public Storage operates in three business segments.

- Public Storage operates 2,787 self-storage facilities in the US, with 198.319 million square feet of space.

- Shurgard Self Storage SA (SHUR.BR) has 253 facilities with 13.799 million square feet of space in seven Western European countries. $PSA owns 35% of Shurgard

- Orange Door, an ancillary brand of Public Storage, provides tenant reinsurance and other related services.

The US operations of the Public Storage brand generates a large majority of the Company’s income.

Up until July 2022 Public Storage also managed commercial properties, through a 41% interest in PS Business Parks Inc, which owns 27.7 million square feet of space in six states. Public Storage sold this interest to affiliates of Blackstone Real Estate for $2.7 billion in April 2022. The sale allows $PSA to focus on its core self-storage and ancillary services businesses.

Public Storage has moved aggressively to leverage technology in support of a traditional business.

- eRental is a digital lease that allows customers to rent online and move in themselves. It accounts for 50% of move-ins.

- Digital Property Access Systems allows direct access to parking gates, doors, and elevators through the Public Storage app.

- Comprehensive mobile app: the highly-reviewed app provides full leasing, account management, customer service, and access functions.

These innovations reduce overhead and provide a superior customer experience, allowing customers to rent and access storage space entirely through the app..

Public Storage added 240 properties with a total of 23 million square feet of storage space in 2021, using acquisitions, development, and redevelopment.

Expansion is continuing in 2022. Since June 30 $PSA has acquired or is under contract to acquire 24 self-storage facilities with 1.7 million square feet of rentable space.

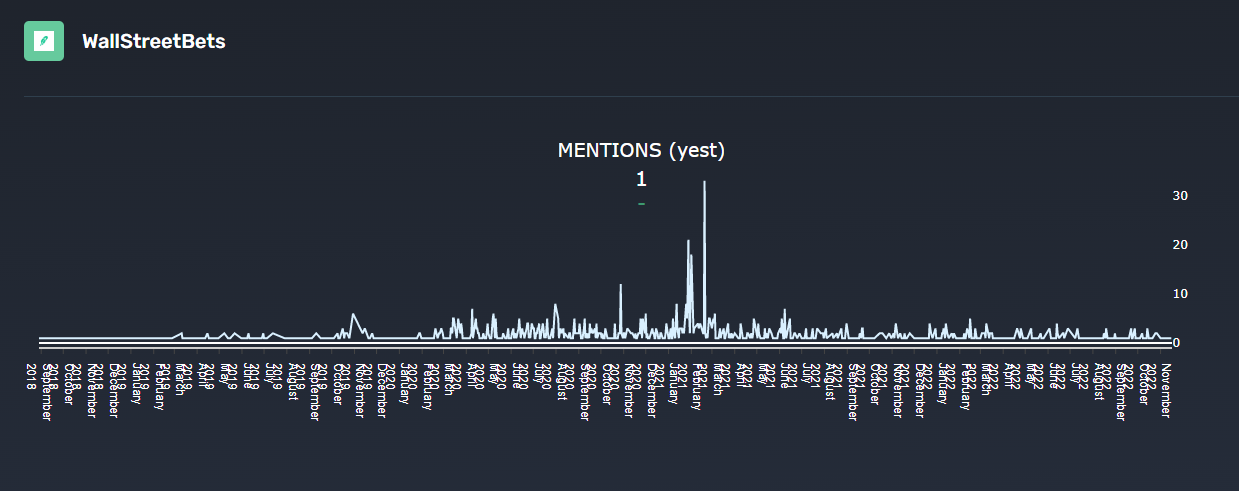

???? What we learned from social media and institutional investment patterns:

$PSA sees minimal discussion on Reddit, and what little there is can be found as a general discussion of REITs and dividend stocks.

This is not surprising. Most REITs are classic “boring stocks”, they aren’t likely to go “to the moon” or experience viral trading. They are not household names or purveyors of the latest technology.

Source: quiverquant.com

There are a few posts on r/stocks and the discussion is generally positive, but there’s too little of it to draw any conclusions. It is reasonable to assume that price movements will not be driven by social media buzz.

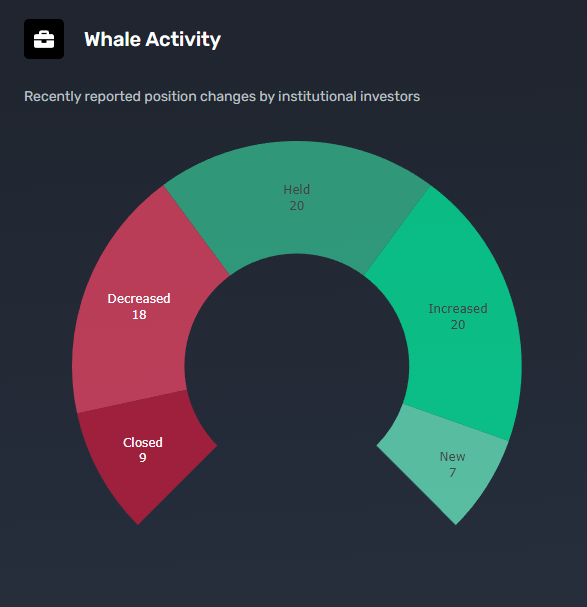

13.58% of $PSA shares are held by insiders, a relatively high figure. 94.01% of the float is held by institutional investors, led by Vanguard and Blackrock. Recent institutional activity has been generally positive:

Source: quiverquant.com

Notable comments from Reddit:

“I have owned them for years and think they are a good buy because people use them in good times and in bad times. When downsizing, for example, people store all their stuff there that won't fit in their new place.

They are also updating their existing facilities to be non-staffed and I'm sure they will keep at this as much as humanly possible. This means that you enter a code to get into the gate, and then enter your code to unlock your storage space, rather than deal with an employee. Having a business that works just fine with no staff on site is incredible and the more they change to be like this, the more profit they will make.”

– kezlorek

“I work for a marketing firm and our biggest client is a self storage company that competes directly with Public Storage. PSA is by far the most popular self storage company on the market. I deal with the pay per click metrics daily and see it myself. I’d go with PSA.”

– WjorgonFriskk

???? Smart Money Signal: Ken Griffin of Citadel has purchased 191,000 shares of $PSA in the last two quarters. Ray Dalio has bought shares in the last four consecutive quarters.

???? Why $PSA could be valuable:

The self-storage market is expected to show a CAGR of 7.53%% through 2027.

Self-storage is traditionally a recession-resistant business, as financially stressed individuals and households move to smaller, more affordable accommodations and look for places to store their belongings. During the 2008-2009 recession, when most commercial real estate saw a 25% to 67% drop in earnings, self-storage saw a 5% gain.

The self-storage market is highly fragmented, with nearly 75% of the market in the hands of small local operators. Size and nationwide reach give Public Storage a substantial advantage. They have the financial capacity to drive acquisitions, property expansion, and property development, and to invest in automated systems that reduce overhead and enhance customer appeal.

The nationwide reach and financial capacity of Public Storage also allow advertising and brand-building on a national scale, something few competitors can match.

Public Storage has invested heavily in technology. As a result, customers can rent space, manage their accounts, and gain secure access to their storage units entirely through a dedicated app. No competitor can match this capacity.

Public Storage has used acquisitions, site expansion, and new site development to expand its total US rental space from 2,429 facilities with 162.047 million square feet of rentable space at the end of 2018 to 2,787 facilities with 198.319 million square feet of rentable space at the end of 2021.

Expansion has continued in 2022: in the third quarter $PSA acquired 24 facilities with 1.7 million square feet of storage space and gained another .5 million square feet from internal development. As of Sept 30, 2022, the Company had 5.1 million square feet of new projects in development.

$PSA’s occupancy rate is currently 94.5%. This is down from 96.8% a year earlier, probably due to the addition of new space, but it remains a very strong figure. An excessively high occupancy rate is not entirely positive, as it leaves no room to accommodate new customers.

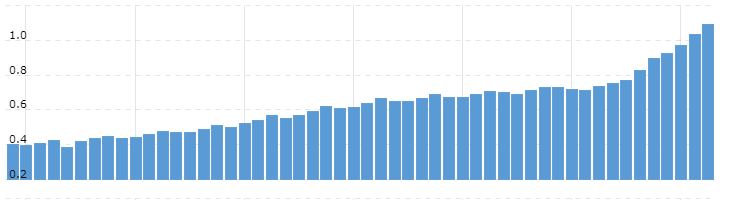

Public Storage revenues have increased consistently, both from same-facility growth and from the addition to new facilities. Same-store net operating income (NOI) was up 17% from the previous year in Q3 2022. Core funds from operations (FFO) a metric frequently used by REITs, increased 20%

Quarterly Revenues (billions):

The surge in EPS is due to the sale of the Company’s 41% interest in PS Business Parks, and will not be repeated.

$PSA boasts an impressive operating margin of 51.1%, with ROE at 47.74%. The Company has a solid cash position, and while it carries substantial debt, like most REITs, its debt-to-equity ratio is lower than that of most competitors. The Company has the capacity to sustain it’s acquisition and development program.

$PSA earnings have beaten consensus analyst estimates for four consecutive quarters.

Shares are trading at 30% below their April 2022 peak despite strong financial performance. The dividend yield currently stands at 2.73%.

18 analysts currently cover $PSA, with a consensus “Buy” rating and an average price target of $359.08, 22.34% above the current price.

⚠️ What the risks are:

1 A substantial debt load. The Company’s long-term debt load has grown from $1.9 billion at the end of 2019 to $6.74 billion in the most recent quarter. This is a typical pattern for REITs, which rely on debt to acquire and expand properties. Rolling over debt could still be a challenge as interest rates rise, especially if the acquisitions are less profitable than expected.

2 Data security and privacy risks. The move to tech-driven systems reduces costs and appeals to customers, but it produces risks. Any data breach leading to the release of customer data or the theft of property could have a serious impact on the Company’s credibility and on customer trust.

3 Development risk. $PSA is aggressively developing new self-storage facilities. Costs may exceed projections, and the space in these facilities is not pre-leased. Development decisions are based on projected demand and the projections may not be accurate.

Bottom line: Public Storage is a conservative, recession-resistant dividend-bearing REIT with a strong financial position. It’s a defensive investment ideally positioned to weather economic storms.