Humana is a leading provider of health insurance plans, primarily under contracts with Medicare and other government programs. It’s well insulated from recession and inflation and showing solid growth.

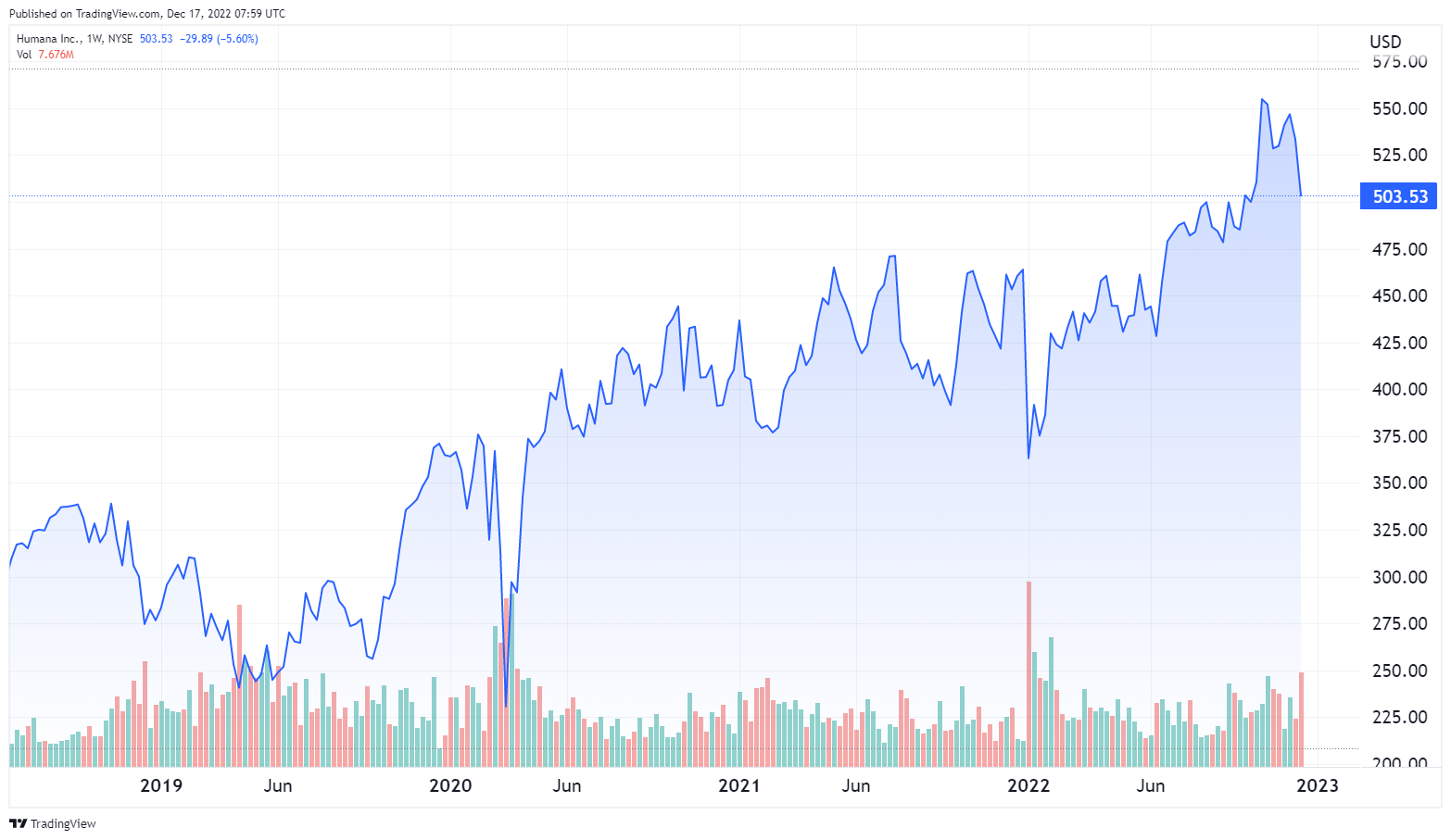

Humana Inc ($HUM)

Source: tradingview.com

???? Summary:

- Share price at the time of writing: $503.53

- Humana is a major provider of health insurance in the US.

- Most Humana revenue comes from contracts with the US government, under Medicare, Medicaid, and the US military’s TRICARE.

- The share price has fallen almost 53% in the last year despite steadily improving performance.

???? What they do:

Humana is one of the largest health plan providers in the US. The Company was founded in 1964 and is based in Louisville, KY.

Humana has approximately 17 million members in its medical benefit plans and another 5 million in specialty product plans covering dental, vision, and other services. 83% of premiums and services revenue come from contracts with the federal government.

15% of premiums and services revenue comes from Medicare Advantage contracts in Florida with the Centers for Medicare and Medicaid Services (CMS).

Humana has three reporting divisions.

- Retail includes products sold on an individual basis, primarily Medicare progams. Humana offers at least one Medicare plan in all 50 states. This segment provides 89.2% of revenue.

- Group and Specialty provides commercial insurance to employers and other groups, including TRICARE contracts with the US military. Along with dental. Vision, and life insurance. The division contributes 8.3% of revenue.

- Healthcare Services includes pharmacy, healthcare provider, and home services to Humana plan holders, including full-service medical centers in nine states. The division provides 2.7% of revenue.

Humana’s retail division provides access to health care services primarily through contracted networks of providers. Services are provided through three models.

- Health Maintenance Organizations (HMOs) provide comprehensive care through a network of participating providers.

- Preferred Provider Organizations (PPOs) allow members to choose any provider, but they may pay more for out-of-network providers.

- Point of Service (POS) plans allow members a range of out-of-network and in-network providers, adding more flexibility.

Humana provides these services primarily to Medicare-eligible individuals through contracts with CMS. Humana provides coverage under CMS contracts to roughly 4,409, 100 individuals.

Humana offers stand-alone prescription drug plans under Medicare Part D in a co-branded offering with Wal-Mart.

HUM provides services to Medicaid-eligible individuals through contracts with state governments in several states, including Florida, Kentucky, Ohio, South Carolina and Wisconsin.

Humana provides insurance to 6 million TRICARE beneficiaries in the East Region under a contract with the US Department of Defense.

In August 2021 Humana acquired Kindred at Home (KAH), the nation’s largest home health and hospice provider. KAH has locations in 40 states, boosting Humana’s effort to provide cost-effective home-based care.

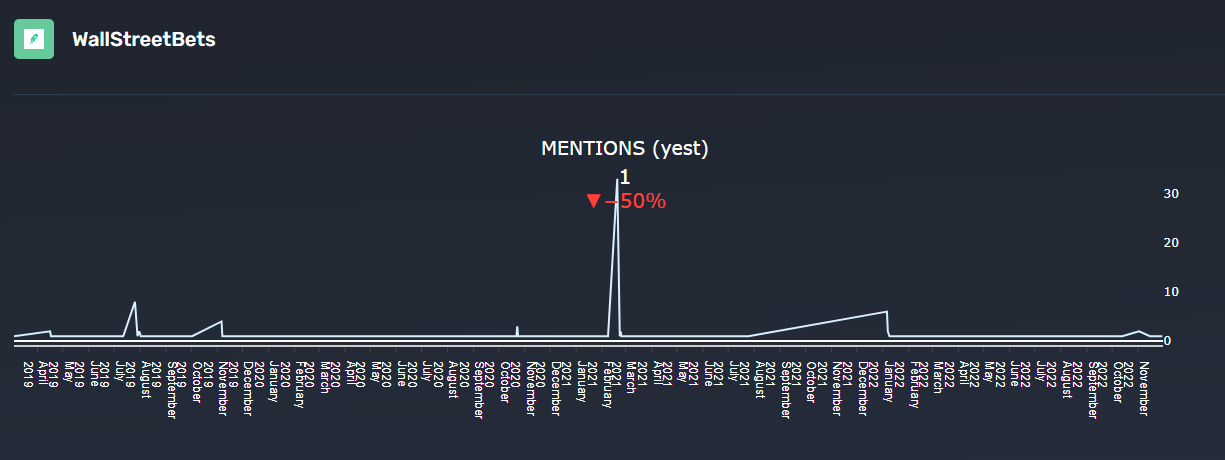

???? What we learned from social media and institutional investment patterns:

Humana receives minimal attention on the main stock discussion forums on Reddit.

Source: quiverquant

Reddit searches indicate that most mentions of $HUM are in the context of a general discussion of dividend stocks, healthcare stocks, or defensive investments rather than in threads dedicated to the Company.

This is expected. Humana is a classic “boring stock” that would not receive significant social media attention even during bull markets when social media chatter is peaking.

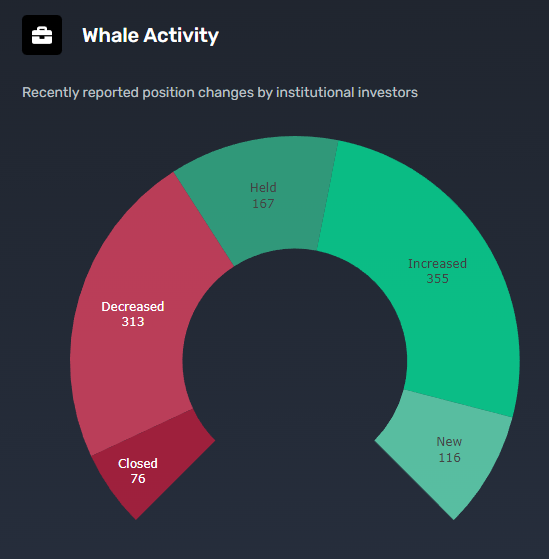

Also as expected, $HUM has a very high percentage of institutional ownership. Over 96% of the float is held by institutional investors. Blackrock and Vanguard lead the pack with over 11 million shares each. Institutional investors show a generally positive trading pattern.

Source: Quiverquant

???? Smart Money Signal ???? Ken Griffin of Citadel has purchased 748,000 shares of $HUM in the last 3 quarters, and now holds a total of 1.15 million shares..

???? Why $HUM could be valuable:

McKinsey estimates that the US national health expenditure will grow at a rate of 7.1% a year through 2027. The US health insurance market in particular is expected to show a CAGR of 9.5% through 2028.

Medicare Advantage plans, which make up a large percentage of Humana’s business, are rapidly gaining in popularity. The Kaiser Family Foundation predicts that per capita Medicare spending will increase 5.1% a year through 2028.

These increases are driven largely by the aging of the Baby Boom generation. Boomers are now aged 58 to 76, meaning that a substantial number are still employed and not yet Medicare-eligible. That will drive growth in Medicare-related spending for close to another decade.

Healthcare is a notably inflation-resistant and recession-resistant business: people need care no matter what economic conditions prevail.

The KAH acquisition dramatically boosted Humana’s home care capacity. The ability to deliver effective home care reduces client dependency on expensive hospital care, reducing the overall cost of care.

$HUM is currently a front runner in the race to acquire Cano Health, one of the nation’s largest providers of primary care to families and seniors. Cano has facilities in California, Florida, Illinois, Texas, and New Mexico. Adding the primary care capacity of Cano to the $HUM package could substantially reduce secondary and tertiary care costs.

$HUM has the right of first refusal over a Cano acquisition under a 2019 agreement.

Humana has boosted its projection for individual Medicare Advantage growth in 2023 from 150,000 – 200,000 to 325,000-400,000. EPS growth is expected to be 11% to 15%.

Revenues have grown steadily and consistently since 2009, and are up 66% in the last 12 months, and share buybacks have reduced the float by 12%, with the combination increasing revenue per share by 90% over the last year.

$HUM has beaten consensus analyst earnings estimates for four consecutive quarters.

Humana’s forward dividend yield is only .6%, but the dividend has grown every 12% to 15% every year since 2017, and the very low 12% payout ratio could easily support a much higher dividend.

Humana’s cash position of $26.68 billion is significantly higher than its $10.83 billion debt.

19 analysts currently cover #HUM. 7 rate it “Strong Buy”, 5 say “Hold”, and 7 say “Hold”. The average price target is $615.18, 22% above the current price.

⚠️ What the risks are:

1 High dependence on government contracts. The rapid growth of Medicare spending may become unsustainable, leading to regulatory changes or even structural changes in the US healthcare system. Such changes could have a dramatic impact on Humana’s business..

2 Contract renewal risk. Humana’s government contracts must be renewed regularly and the company faces a detailed performance review with each renewal. Any failure to meet standards could result in contracts being terminated.

3 Underwriting risk. A large portion of revenues are paid out to cover member claims. Humana must effectively assess risk and set premiums appropriately. Laws prohibit consideration of pre-existing conditions in setting premiums in some cases, increasing this risk. Failure to anticipate and correctly assess risk would have a material impact on results.

Bottom line: Humana is a highly secure defensive stock that is very well positioned to endure and prosper in any economic conditions. It also combines a high degree of resilience with strong growth, something that’s not present in many fundamentally defensive stocks.